Uniswap V3 Simulation

Here we utilize UniswapPy to simulate an order book in Uniswap V3

Medium Article: How to Simulate a Uniswap V3 Order Book in Python

To download notebook to this tutorial, see here

📘 Notable Classes

Class: 📘

defipy.math.model.BrownianModelPurpose: Geometric Brownian process.

Methods:

gen_gbms(mu: float, sigma: float, n_step: int, T: int = 1)Parameters:

mu: asset drift (float).sigma: asset volatility (int).n_step: number of steps. (int).T: time unit (optional) (int).

Class: 📘

defipy.math.model.TokenDeltaModelPurpose: Random sample of Gamma distribution representing an experimental token amount.

Methods:

delta(p: int = 1)Parameters:

p: buy/sell probability associated (buy = 1, sell = -1, optional) (int).

Class: 📘

defipy.analytics.simulate.CorrectReservesPurpose: Applies

SolveDeltasto Correct x/y reserve amounts so that price reflects desired input price; in the marjority of cases, the input price would be the most recent outside market price .Methods:

delta(price: float, lwr_tick: int = None, upr_tick: int = None)Parameters:

price: token price (int).lwr_tick: Lower tick of the position. (optional) (int).upr_tick: Upper tick of the position. (optional) (int).

[1]:

from defipy import *

import pandas as pd

import seaborn as sns

import matplotlib.pyplot as plt

user_nm = MockAddress().apply()

eth_amount = 100

tkn_amount = 1000

fee = UniV3Utils.FeeAmount.MEDIUM

tick_spacing = UniV3Utils.TICK_SPACINGS[fee]

Simulate prices

Simulate prices using a geometric brownian motion process

[16]:

n_steps = 1000

start_price = eth_amount/tkn_amount

mu = 0.1; sigma = 0.5

n_paths = 1

b = BrownianModel(start_price)

p_arr = b.gen_gbms(mu, sigma, n_steps, n_paths)

exp_p_arr = np.median(p_arr, axis = 1)

accounts = MockAddress().apply(50)

Setup pool

[17]:

eth = ERC20("ETH", "0x09")

tkn = ERC20("TKN", "0x111")

exchg_data = UniswapExchangeData(tkn0 = eth, tkn1 = tkn, symbol="LP",

address="0x011", version = 'V3',

tick_spacing = tick_spacing,

fee = fee)

factory = UniswapFactory("ETH pool factory", "0x2")

lp = factory.deploy(exchg_data)

lwr_tick = UniV3Helper().get_price_tick(lp, -1, 10, 1000)

upr_tick = UniV3Helper().get_price_tick(lp, 1, 10, 1000)

Join().apply(lp, user_nm, eth_amount, tkn_amount, lwr_tick, upr_tick)

lp.summary()

Exchange ETH-TKN (LP)

Real Reserves: ETH = 96.70469739529014, TKN = 1000.0

Gross Liquidity: 6440.3320664241655

Simulate liquidity pool

[18]:

arb = CorrectReserves(lp, x0 = 1/exp_p_arr[0])

p_intervals = [500, 800, 1000, 1200, 1500, 1700, 2000]

lp_prices = [lp.get_price(tkn)]

lp_liquidity = [lp.total_supply]

lp_swaps = []; lp_net_deposits = [];

for k in range(1, n_steps):

p = 1/exp_p_arr[k]

arb.apply(p, lwr_tick, upr_tick)

select_tkn = EventSelectionModel().bi_select(0.5)

rnd_add_amt = TokenDeltaModel(25).delta()

rnd_swap_amt = TokenDeltaModel(15).delta()

user_add = random.choice(accounts)

user_swap = random.choice(accounts)

p_interval = random.choice(p_intervals)

lwr_tick = UniV3Helper().get_price_tick(lp, -1, lp.get_price(eth), p_interval)

upr_tick = UniV3Helper().get_price_tick(lp, 1, lp.get_price(eth), p_interval)

if(select_tkn == 0):

AddLiquidity().apply(lp, eth, user_add, rnd_add_amt, lwr_tick, upr_tick)

out = Swap().apply(lp, eth, user_swap, rnd_swap_amt)

else:

AddLiquidity().apply(lp, tkn, user_add, p*rnd_add_amt, lwr_tick, upr_tick)

out = Swap().apply(lp, tkn, user_swap, p*rnd_swap_amt)

lp_prices.append(lp.get_price(tkn))

lp_liquidity.append(lp.total_supply)

lp_swaps.append(rnd_swap_amt)

lp_net_deposits.append(rnd_add_amt)

lp.summary()

Exchange ETH-TKN (LP)

Real Reserves: ETH = 153089.57969951717, TKN = 1063580.263806977

Gross Liquidity: 6723644.391607661

Construct order book

[19]:

liquidity = {}

df_liq = pd.DataFrame(columns=['tick', 'price', 'liquidity'])

for k, pos in enumerate(lp.ticks):

price = UniV3Helper().tick_to_price(pos)

liq = lp.ticks[pos].liquidityGross/10**18

df_liq.loc[k] = [pos,price,liq]

center_pos = UniV3Helper().price_to_tick(lp.get_price(eth))

price = lp.get_price(tkn)

df_liq.loc[k+1] = [center_pos,price,0]

df_liq.sort_values(by=['price'], inplace=True)

df_liq.reset_index(drop=True, inplace=True)

side_arr = []

for tick in df_liq['tick'].values:

if (tick > center_pos):

side_arr.append('asks')

elif (tick < center_pos):

side_arr.append('bids')

else:

side_arr.append('center')

df_liq['side'] = side_arr

idx = df_liq.index[df_liq['side'] == 'center']

df_liq.drop(idx[0], inplace=True)

[20]:

df_liq

[20]:

| tick | price | liquidity | side | |

|---|---|---|---|---|

| 1 | 15000.0 | 4.481353 | 21.875455 | bids |

| 2 | 15180.0 | 4.562744 | 2302.827924 | bids |

| 3 | 15300.0 | 4.617824 | 3.923965 | bids |

| 4 | 15360.0 | 4.645612 | 272.986987 | bids |

| 5 | 15540.0 | 4.729986 | 4858.284512 | bids |

| ... | ... | ... | ... | ... |

| 166 | 25200.0 | 12.427031 | 742.064919 | asks |

| 167 | 25260.0 | 12.501813 | 474.771564 | asks |

| 168 | 25440.0 | 12.728872 | 447.693367 | asks |

| 169 | 25500.0 | 12.805471 | 457.990880 | asks |

| 170 | 25620.0 | 12.960055 | 366.017072 | asks |

170 rows × 4 columns

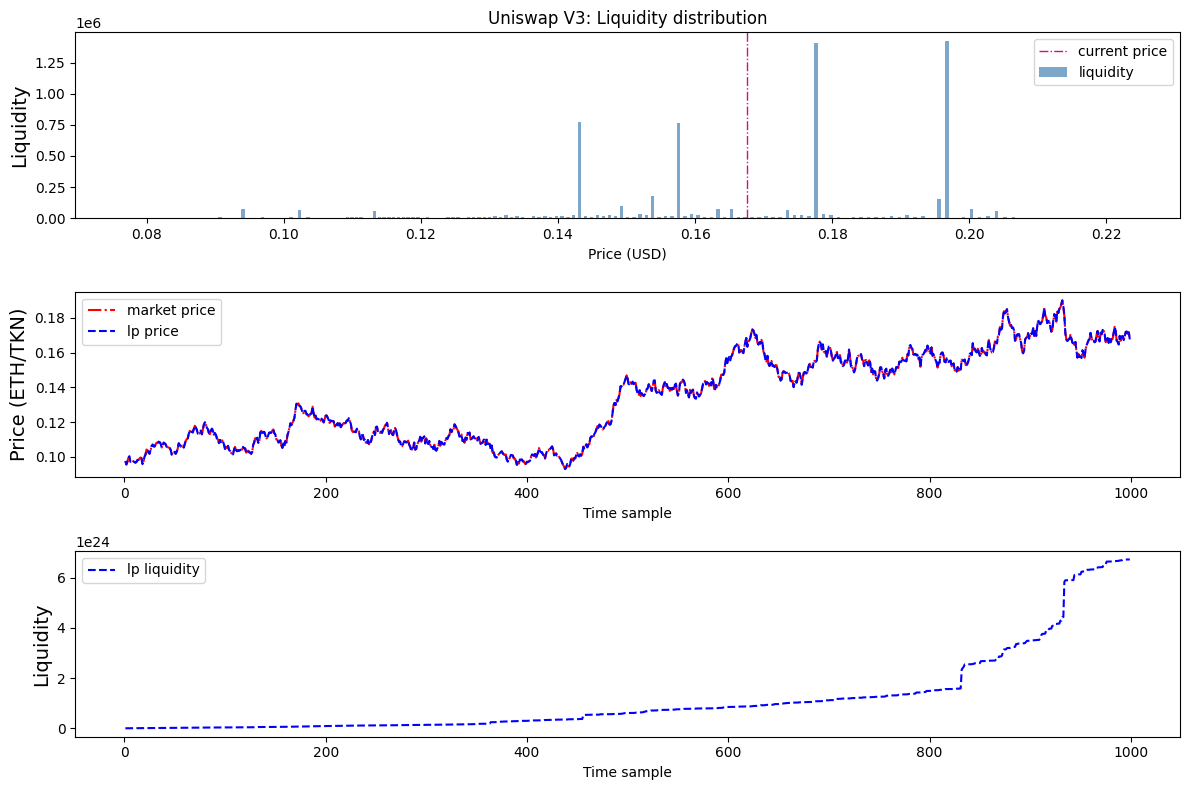

Review simulation output

[21]:

fig = plt.figure(figsize = (10, 5))

current_price = lp.get_price(tkn)

prices = 1/df_liq['price'].values

liquidity = df_liq['liquidity'].values

fig, (book_ax, price_ax, liq_ax) = plt.subplots(nrows=3, sharex=False, sharey=False, figsize=(12, 8))

book_ax.bar(prices, liquidity, color ='steelblue', width = 0.0005, label = 'liquidity', alpha=0.7)

book_ax.axvline(x=current_price, color = 'mediumvioletred', linewidth = 1, linestyle = 'dashdot', label = 'current price')

book_ax.set_xlabel("Price (USD)", size=10)

book_ax.set_ylabel("Liquidity", size=14)

book_ax.set_title("Uniswap V3: Liquidity distribution")

book_ax.legend()

x_val = np.arange(0,len(p_arr))

price_ax.plot(x_val[1:-1], p_arr[1:-1], color = 'r',linestyle = 'dashdot', label='market price')

price_ax.plot(x_val[1:-1], lp_prices[1:], color = 'b',linestyle = 'dashed', label='lp price')

price_ax.set_ylabel('Price (ETH/TKN)', size=14)

price_ax.set_xlabel('Time sample', size=10)

price_ax.legend()

liq_ax.plot(x_val[1:-1], lp_liquidity[1:], color = 'b',linestyle = 'dashed', label='lp liquidity')

liq_ax.set_ylabel('Liquidity', size=14)

liq_ax.set_xlabel('Time sample', size=10)

liq_ax.legend()

plt.tight_layout()

<Figure size 1000x500 with 0 Axes>

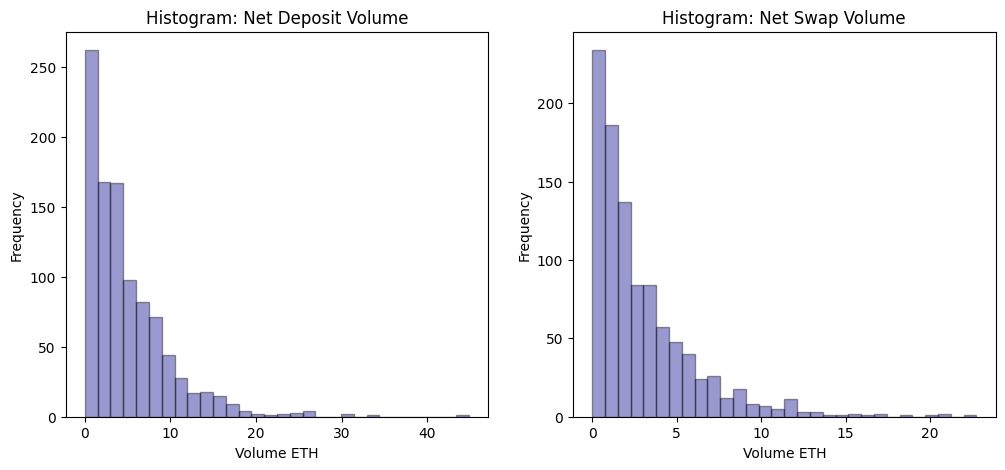

[22]:

fig, ax = plt.subplots(1, 2, figsize=(12,5))

sns.distplot(lp_net_deposits, hist=True, kde=False, bins=int(30), color = 'darkblue',

hist_kws={'edgecolor':'black'}, kde_kws={'linewidth': 2}, ax=ax[0])

ax[0].set_title('Histogram: Net Deposit Volume')

ax[0].set_xlabel('Volume ETH')

ax[0].set_ylabel('Frequency')

sns.distplot(lp_swaps, hist=True, kde=False, bins=int(30), color = 'darkblue',

hist_kws={'edgecolor':'black'}, kde_kws={'linewidth': 2}, ax=ax[1])

ax[1].set_title('Histogram: Net Swap Volume')

ax[1].set_xlabel('Volume ETH')

ax[1].set_ylabel('Frequency')

[22]:

Text(0, 0.5, 'Frequency')

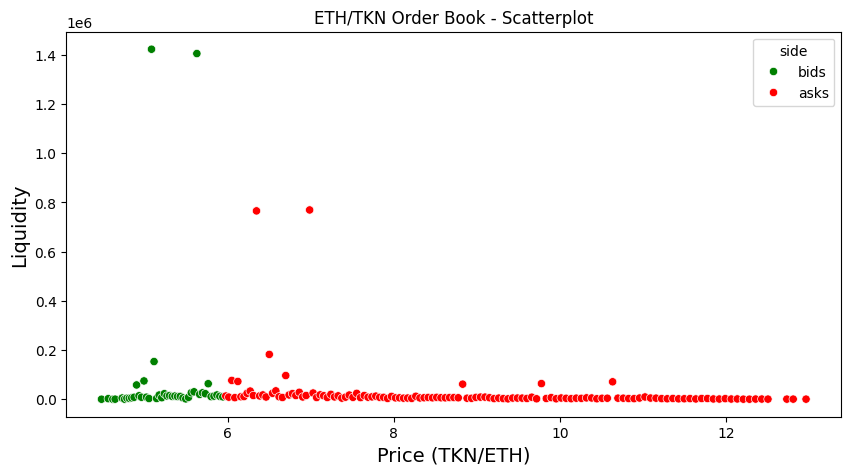

Plot order book

[23]:

fig, ax = plt.subplots(figsize = (10, 5))

ax.set_title(f"ETH/TKN Order Book - Scatterplot")

sns.scatterplot(x="price", y="liquidity", hue="side",

data=df_liq, ax=ax, palette=["green", "red"])

ax.set_xlabel("Price (TKN/ETH)", fontsize = 14)

ax.set_ylabel("Liquidity", fontsize = 14)

[23]:

Text(0, 0.5, 'Liquidity')

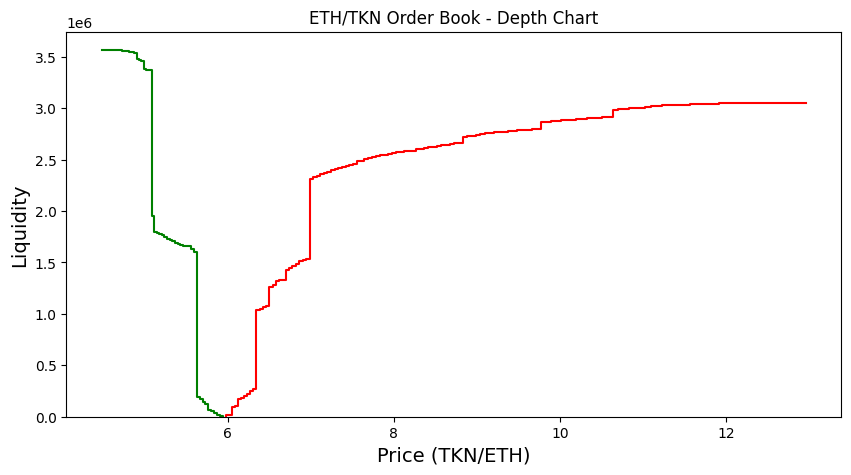

[24]:

fig, ax = plt.subplots(figsize = (10, 5))

ax.set_title(f"ETH/TKN Order Book - Depth Chart")

sns.ecdfplot(x="price", weights="liquidity", stat="count",

complementary=True, data=df_liq.query("side == 'bids'"),

color="green", ax=ax)

sns.ecdfplot(x="price", weights="liquidity", stat="count",

data=df_liq.query("side == 'asks'"), color="red",

ax=ax)

ax.set_xlabel("Price (TKN/ETH)", fontsize = 14)

ax.set_ylabel("Liquidity", fontsize = 14)

[24]:

Text(0, 0.5, 'Liquidity')